From factory to field: How energy storage innovations are responding to Europe’s C&I segment

EUPD Research says the growth of the C&I segment in Europe's energy storage market is driving new investment opportunities. The Bonn-based research group has explored what this growth means for both manufacturers and investors, as well as how manufacturers are addressing the needs of C&I installers and customers.

EUPD Research says the growth of the C&I segment in Europe's energy storage market is driving new investment opportunities. The Bonn-based research group has explored what this growth means for both manufacturers and investors, as well as how manufacturers are addressing the needs of C&I installers and customers.

Market dynamics, C&I momentum and installer demands

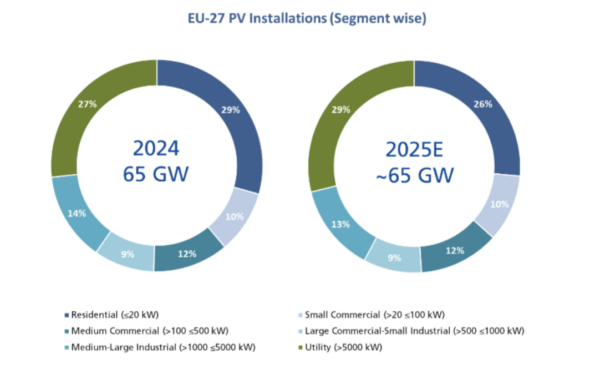

The European solar market is undergoing a notable redistribution of installed capacity. While the residential segment has experienced a surge after the energy crisis, 2025 projections point to increasing momentum in the C&I (commercial & industrial) and utility segments. The slowdown in residential growth is mainly attributed to high interest rates, stabilized electricity prices and the phase-out of support schemes such as Italy’s superbonus tax credit. With 65 GW installed in 2024 and the same (or even slightly less) is estimated for 2025, Europe’s solar market is entering a phase of flat growth.

Source: EUPD Global Energy Transition GET-Matrix©

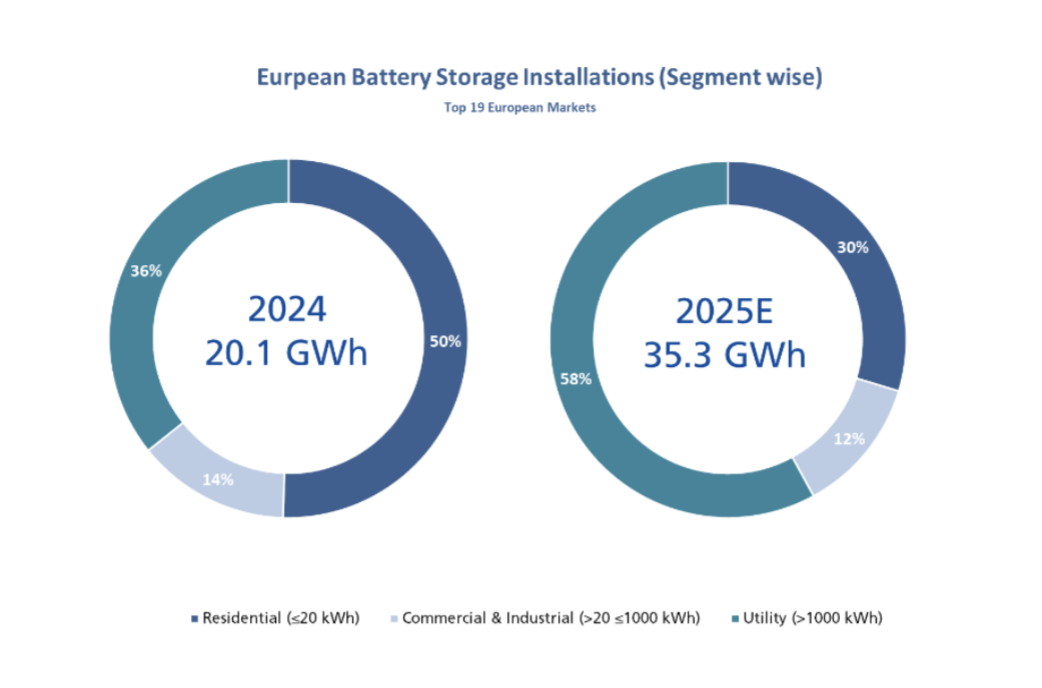

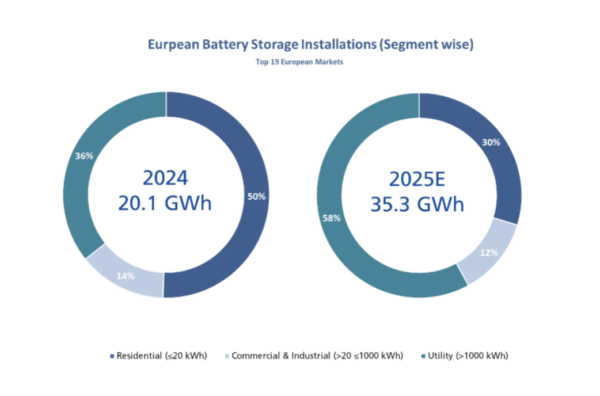

A similar segmental evolution is unfolding in the Electrical Energy Storage (EES) market. Installed storage capacity across Europe (top 19 European Markets) is expected to grow from 20.1 GWh in 2024 to 35.3 GWh in 2025. Residential storage’s share is projected to drop from 50% to 30%, while the C&I segment will represent 12%, a slight decline in share, but an increase in absolute volume due to overall market expansion.

Source: EUPD Global Energy Transition GET-Matrix©

Such an environment demands urgent attention to two critical developments:

1. The growth of the C&I segment is driving new investment opportunities while simultaneously introducing new risks (addressed in EUPD Research Brand Leadership and Sustainability Rating/BLSR, see here).

2. Innovation has emerged as a key lever for unlocking value, enhancing margins, and building customer trust, essential factors for attracting fresh investment, particularly in the residential and C&I sectors.

These trends are clearly reflected in the activities of downstream market players. In France, 50% of installers surveyed in EUPD Research’s PV | EES InstallerMonitor© 2024/2025 reported being active in the C&I segment. When measured by total installed capacity, this share rises to 72%, underscoring the growing relevance of C&I projects. In Germany, the figures are even higher. Additionally, European installers expressed a strong demand for increased innovation; both developments will be explored in more detail below.

What C&I growth means for manufacturers and investors

C&I growth in Europe presents major opportunities, but manufacturers and investors must recognize that the continent is a patchwork of diverse markets, not a unified whole. Therefore, a clear criteria-based tiering of markets based on segmental market historical and forecast developments, presence of support schemes, electricity tariffs and net benefits etc. is critical for better results. Without tierisation, strategies risk being misaligned with local realities. Targeted insights enable smarter investments and more effective market entry.

Furthermore, as storage projects scale into the C&I segment, the risk environment shifts considerably. Unlike residential systems, C&I installations require larger capital outlays, longer planning cycles, and greater operational accountability. This raises the stakes for selecting reliable technology partners. Brand trust, installer satisfaction, Net Promoter Scores, and the ability to demonstrate sustained R&D investments through patents, certifications, and technological resilience: all of these serve as the decisive factors. In this context, choosing the right manufacturer is not just about performance or pricing but also about minimizing long-term risk.

To support stakeholders in navigating these growing complexities, EUPD Research introduced the Brand Leadership and Sustainability Rating (BLSR) framework earlier this year. Designed to evaluate manufacturers beyond financial, price and technical metrics alone, BLSR offers a holistic benchmarking tool that addresses both investor needs for brand security and manufacturer needs for strategic improvement. It enables risk-averse brand selection via comprehensive ESG analysis, including R&D investment, patent acquisition and installer reputation, which together serve as risk mitigator for current and future C&I projects.

What are European installers asking for?

Since the flat growth in the PV market clearly casts its shadow on EES growth, majority of the C&I and residential installers are prioritizing innovation. In Belgium, 29% of the surveyed installers cited product innovation as a critical need, with similarly strong responses in the UK (23%), France (21%), and other markets. The demand calls for innovation in integration, safety, and scalability. As one French installer put it “I’d like to see more innovation and better design”; an Italian installer said that “[they] would appreciate continued developments in the seamless integration of inverters and energy storage systems.” In the DACH region (Germany, Austria and Switzerland), there was a good deal of installer voice for more system integration and smaller system sizes. As one Swiss installer put it: “I would like to see the storage units designed for maximum performance in the smallest possible space and thus optimized” and a German installer asked for more “module efficiency and storage energy density (need to be increased)”.

Bridging the gap: Innovations addressing the needs of C&I installers and customers

As we head into an energy landscape where C&I storage takes a more central role, innovation is no longer a bonus, but rather critical for survival. Direct feedback from installers across key European markets consistently points to a few common demands: greater integration between storage systems and inverters, more compact designs, enhanced safety features, and seamless compatibility with smart energy systems. These requests reflect a growing need for commercial-ready storage solutions that reduce planning and installation complexity while delivering long-term reliability.

Recognizing these evolving needs, the EUPD Research Top Innovation Awards (TIA) was established to spotlight market-ready solutions that directly address installer and system integration challenges. Each year, EUPD Research evaluates hundreds of technology entries across solar, storage and inverter with an expert jury and installer panel identifying standout innovations. Among the most compelling TIA recipients are those that offer modular, intelligent, and easy-to-deploy systems. For example, BYD’s Modular Storage Platform (6–90 kWh) features high-density LFP cells, tool-free installation, and smart diagnostics, ideal for space- and cost-sensitive projects. GivEnergy’s Commercial All-in-One integrates battery, inverter, and EMS with AI optimization in a scalable, plug-and-play format. WeCo’s 5K0 SMART emphasizes safety with built-in fire suppression, seismic protection, and thermal control in a modular system. FOX ESS’s Integrated Residential System combines inverter, battery, and EMS in one compact, scalable unit. These innovations simplify installation, enhance performance and interoperability, and meet diverse C&I and residential needs. A win-win for all sides!

Investor and manufacturer alignment in the C&I storage

As Europe’s energy storage market pivots toward the C&I segment, both investors and manufacturers face a rapidly changing landscape. Flat growth in PV and storage (mostly residential) is driving greater demand for precise market targeting via detailed segmental tierisation and innovation in system design, integration, operational safety, and smart systems: as clearly echoed by installers across the continent. With rising investment risks and technical complexity in C&I deployments, decision-making requires stronger evaluation tools that consider not just technical performance but also brand reliability, installer trust, and innovation depth. Now is the time for the entire PV and storage industry to foster seamless coordination among all stakeholders, especially among manufacturers, installers and prosumers, to unlock win-win outcomes. This is the way!

Authors: Markus A.W. Hoehner, Varun Mahankali and Ali Arfa

Markus A.W. Hoehner is the Founder, President and Chief Executive Officer of Hoehner Research & Consulting Group and EUPD Research. He has been active in top-level research and consulting, focusing on cleantech, renewable energy, and sustainable management for more than three decades. He can be reached at m.hoehner@eupd-research.com.

Varun Mahankali is a Senior Analyst and the Manager of the Top Innovation Awards at EUPD Research. He has over five years of experience in clean tech research and consulting. His expertise spans market intelligence, innovation analysis and consulting within the renewable energy sector. He can be reached at v.mahankali@eupd-research.com.

Ali Arfa is a Senior Data Manager at EUPD Research. He is a graduate of the University of Bonn and with a background in European and North American politics. His expertise encompasses market research, policy development, and stakeholder analysis. His particular focus is on solar energy, energy storage, and strategic consultation. He can be reached at a.arfa@eupd-research.com.

What's Your Reaction?