Revised solar stock investment risks

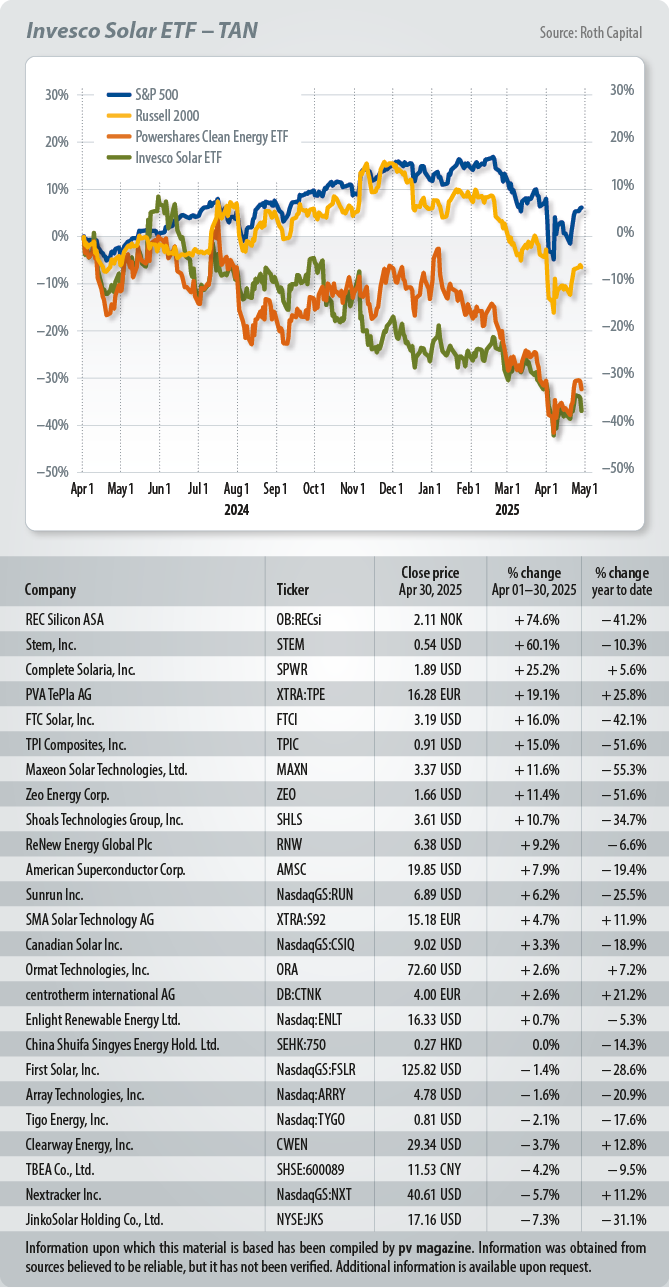

The Invesco Solar ETF (TAN) underperformed the S&P 500 and Dow Jones Industrial Average (DJIA) in April 2025. Jesse Pichel of Roth Capital Partners attributes this to concern over proposals included in the U.S. administration’s budget reconciliation bill that could be detrimental to the solar industry.

The Invesco Solar ETF (TAN) underperformed the S&P 500 and Dow Jones Industrial Average (DJIA) in April 2025. Jesse Pichel of Roth Capital Partners attributes this to concern over proposals included in the U.S. administration’s budget reconciliation bill that could be detrimental to the solar industry.

From pv magazine 6/25: The Hunt For High Efficiency

The Invesco Solar ETF decreased by 7.9% in April, while the S&P 500 fell by 1.1%. The DJIA was down 3.1%. The top three performing US solar stocks for the month of April were Stem Inc. (+60%), Complete Solaria Inc. (+25%), and FTC Solar Inc. (+16%).

The three underperforming U.S. solar stocks for April 2025 were Sunnova Energy International Inc. (-43%), Daqo New Energy Corp. (-30%), and Enphase Energy Inc. (-29%).

Residential solar stocks slid 6.2% in April and have plunged 38.1% for the year to date. Utility-scale solar equipment stocks edged up 4% for the month of April but have fallen 23% year to date. Independent power producer (IPP) stocks were down 5% in April for a year-to-date decline of 5%.

The U.S. House Rules Committee’s amendment to the budget reconciliation bill poses a greater threat to the solar industry than initially expected. Contrary to assumptions that the first draft would be the harshest, the latest version introduces provisions with significant negative implications.

Most notably, the bill aims to deny residential leasing companies access to Section 48E investment tax credits and immediately sunset Section 25D, the residential solar credit for loan and cash purchases. Together, these changes could severely impact the residential solar market beginning Jan. 1, 2026, posing major risks for the broader segment.

For utility-scale solar, the amendment removes the phase-out structure for Section 48E and Section 45Y tax credits. Additionally, the construction start date for projects involving “material assistance” from foreign entities of concern (FEOCs) would be pulled forward to year-end 2025, tightening compliance timelines.

The one relative positive is that 45X manufacturing credits and their phase-out timelines remain unchanged from the earlier draft. Overall, the revised bill significantly raises near-term risk, warranting close attention as negotiations continue.

Jesse Pichel, Roth Capital Partners

What's Your Reaction?