Solar farms in southern Australia face major curtailments by 2027

New large-scale solar farms in southeastern Australia could be forced to curtail up to two-thirds of their power generation by 2027 due to delays in energy transmission infrastructure projects, according to new analysis from the Australian Energy Market Operator (AEMO).

New large-scale solar farms in southeastern Australia could be forced to curtail up to two-thirds of their power generation by 2027 due to delays in energy transmission infrastructure projects, according to new analysis from the Australian Energy Market Operator (AEMO).

The AEMO has forecast that major solar farms in Victoria and South Australia could be forced to shut off 35% of their capacity by 2027 while several may be forced to shed more than 65% of their generated power as transmission project delays cause major bottlenecks on the grid.

AEMO’s 2025 Enhanced Locational Information (ELI) report highlights increasing locational risks and opportunities across the National Electricity Market (NEM), with a focus on curtailment, congestion, and hosting capacity.

The report shows that delays for several major transmission projects, including the AUD 3.3 billion ($2.17 billion) VNI West project, a 500 kV double circuit transmission line connecting the New South Wales (NSW) and Victorian energy grids, will severely curtail the amount of energy generated by renewable energy projects over the next two years.

“While some locations have not seen heavy congestion historically, they are nearing their current network limits and additional capacity may result in new areas of congestion,” the report says, noting that some locations are already reaching “significant levels” of congestion and curtailment.

The report shows that in 2024, more than 50% of all grid-scale solar and wind generation experienced network-driven curtailment of less than 1%. Grid-scale solar generation across the NEM jurisdictions averaged 4.5%, while several utility-scale solar PV power plants experienced “very high levels” of curtailment above 25%.

“High curtailment was mainly concentrated in specific areas (particularly western NSW and northwest Victoria) and illustrates that most transmission lines did not experience significant congestion,” said AEMO. “The most severe network congestion arose in areas with high levels of generation connected in locations that were originally designed to service demand rather than supply. These high network congestion areas broadly overlap with the areas experiencing high levels of generation curtailment.”

AEMO warned that curtailment levels across the NEM are expected to rise in the near term, reflecting the mismatch between renewable generation capacity and transmission infrastructure development timelines.

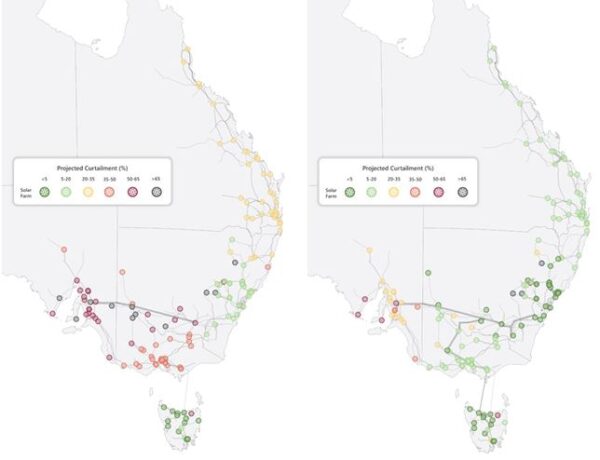

Image: AEMO

Image: AEMO

Analysis of hypothetical new 300 MW solar developments by AEMO shows most will have a shut-off rate of more than 35% by 2027, with that figure exceeding 65% for some projects,

“Projected curtailment is particularly high in South Australia and Victoria in the near term, as these regions are further progressed in the renewable transition, and each further increase in capacity is more heavily curtailed by minimum security and export limitations,” the report says.

AEMO said improvements are expected in the medium term (2030-2035) based on new transmission projects being delivered, and as investment is made to meet required system security services that would begin to relax system security constraints.

Merryn York, AEMO executive general manager of system design, said opportunities exist in all NEM regions for renewable and firming projects but building a reliable and efficient electricity system depends on investing in the right places.

“This report presents key locational data to help investors understand where their projects are most likely to succeed, and where challenges, such as network congestion, curtailment, or energy losses, may arise,” she said. “Not all locations are equal, and geographic network conditions must be a critical part of investment decisions.”

The report shows that as of April 2025, there were approximately 20 GW of projects currently at the application to connect stage, as well as the 300 GW of proposed future projects.

AEMO said to improve their chances of success, investors will need to consider factors such as access to high-quality renewable resources, network congestion, network losses, security requirements, future network changes, and competing projects nearby.

What's Your Reaction?