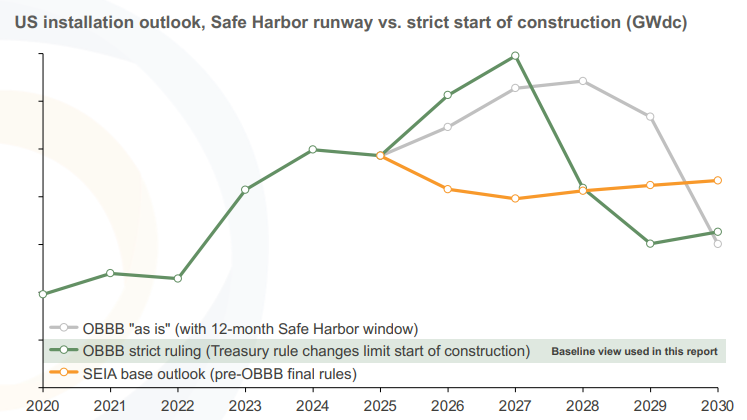

US may lose 60 GW solar pipeline under stricter tax credit rules

Clean Energy Associates (CEA) forecasts a significant drop in solar installations if the US Department of the Treasury strictly enforces an executive order from the White House related to timelines for tax credit eligibility.

Clean Energy Associates (CEA) forecasts a significant drop in solar installations if the US Department of the Treasury strictly enforces an executive order from the White House related to timelines for tax credit eligibility.

From pv magazine USA

The United States could lose 60 GW of planned solar installations through 2030 if the US Department of the Treasury enforces a strict interpretation of the “start of construction” qualifier for the clean energy Investment Tax Credit and Production Tax Credit, according to Clean Energy Associates.

A July 8 executive order from President Donald Trump instructed the Department of the Treasury to tighten restrictions on solar tax credits.

Under the new Republican budget, solar projects that reached “start of construction” within 12 months of enactment, or were “placed in service” by 2028, are eligible for the 45Y Production Tax Credit (PTC) and the 48E Investment Tax Credit (ITC). Such projects would be eligible for the credits under a safe harbor provision.

CEA said strict start-of-construction language could derail about 60 GW projects hoping to take advantage of safe harboring credits until 2030.

The executive order directs the Treasury to restrict safe harboring of projects, tightening interpretation of the “beginning of construction” language. The order requires that a “substantial portion” of a project must be built to secure credits. The order requires the Treasury to enforce this within 45 days of the enactment of the congressional budget bill.

Keith Maritn, partner at Norton Rose Fulbright, said to qualify for safe harbor designation, projects likely will need to “incur” at least 5% of the project’s cost.

“Costs are usually incurred only as the developer takes delivery of equipment or services, with one exception. A payment for specific equipment or services by the deadline counts if delivery is reasonably expected within three and a half months. There are nuances about counting payments for services,” said Martin.

The other path to qualification, he said, is to start “physical work of a significant nature” at the project site on the portions of the project eligible for the 48E credit.

“For years, developers and investors have relied on these rules to qualify projects under the ITC/PTC framework, even when [commercial operation date] occurs years later,” said Peter DeFazio, managing partner, Greenprint Capital. “If interpreted narrowly, projects that haven’t meaningfully advanced beyond paper progress – even with a 5% basis spend – could lose eligibility.”

DeFazio said if the application of this stricter interpretation is retroactive, the fallout would ripple across billions in project pipeline capital. He urged developers to reassess safe harbor assumptions, adjust notice-to-proceed schedules, and evaluate potential portfolio risks.

The early loss of tax credits are expected to deal long-term damage to the industry. Wood Mackenzie forecast 10-year installations could decrease 17%, reaching volumes as low as 375 GW for the decade.

“Permitted projects are well-positioned, but unpermitted developments face growing uncertainty as permitting bottlenecks threaten to push completion dates outside eligibility windows,” said Wood Mackenzie.

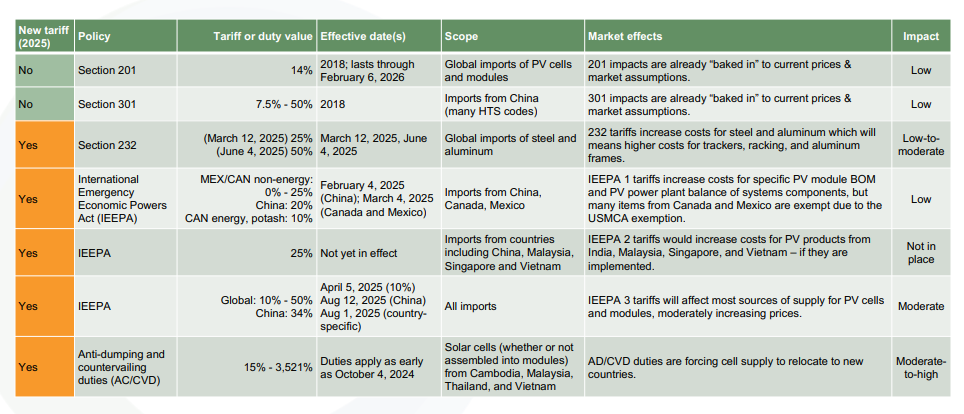

CEA said Trump could take other anti-solar actions, such as pushing for punitive tariffs on equipment, like the far-reaching polysilicon Section 232 tariffs, have the Treasury revise qualification methods, or set additional requirements for project developers.

Tariff enforcement also remains an ongoing threat to solar project development. CEA said PV module, bill of materials, and power plant components could face up to five different tariffs. A summary table is shown below.

What's Your Reaction?