Polysilicon prices in a fragile balance

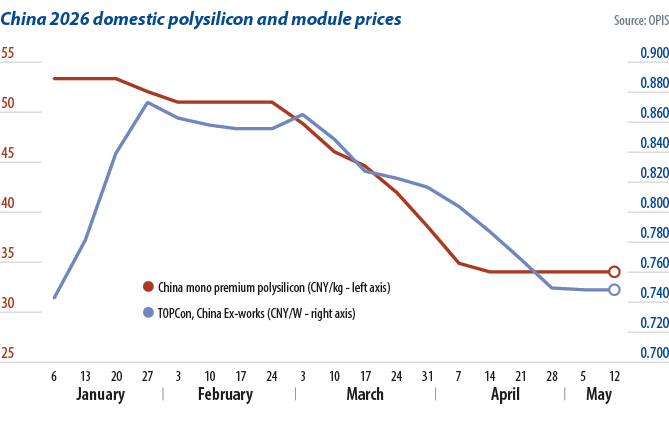

China’s photovoltaic market has shown tentative signs of stabilization over the past month, following an extended period of sharp price declines across the supply chain. The China Mono Premium – OPIS’ assessment for mono-grade polysilicon used in n-type ingot production – remained unchanged for a fourth consecutive week at CNY 34.071 ($5)/kg, or CNY 0.072/W. Before this stabilization, the benchmark had declined continuously for several weeks beginning in late February, falling by more than 33% from end-February levels.

Prices for non-China polysilicon (left axis) have stabilized since April 2026. Future development in this sector will depend on decisions regarding access to the US market (right axis) for overseas materials.

Industry participants generally attributed the recent improvement in market sentiment to a photovoltaic industry symposium held in April to discuss standardizing market competition. This signaled growing policy attention toward the downstream segment of the photovoltaic supply chain and potential adjustments to module tender mechanisms.

Nevertheless, polysilicon producers cautioned that recent industry meetings have so far generated mainly sentiment-driven reactions, while concrete implementation measures remain absent. Structural pressure remains significant. According to the Silicon Branch of the China Nonferrous Metals Industry Association, China’s polysilicon production reached approximately 82,500 metric tons (MT) in April, while inventories increased by another 6,600 MT during the month. Total industry-wide polysilicon inventories were estimated at around 506,000 MT at the end of April.

Reports from one polysilicon producer highlighted the imbalance between production and downstream demand in its first-quarter results. It reported polysilicon output of 43,400 MT, up 74.9% year on year, while sales volumes fell sharply by 84% to only 4,500 MT, implying roughly 40,000 MT of additional inventory accumulation during the quarter.

Sources believe it may take more than two years to gradually absorb the inventory overhang and that a prolonged period of polysilicon prices below CNY 35/kg, potentially extending beyond 2026, may be required to force higher-cost capacity exits and restore healthier supply-demand fundamentals.

Demand also continues to weaken. China’s National Energy Administration reported first-quarter solar installations of 41.39 GW, down 31% year on year, reinforcing industry expectations that China’s solar installation demand may decline in 2026. Market participants added that demand from large utility-scale projects has yet to show meaningful recovery, despite such projects typically accelerating during the second quarter.

Reflecting the weak downstream environment, OPIS assessed ex-works China tunnel oxide passivated contact (TOPCon) module prices at CNY 0.749 ($0.11)/W as of May 12, down 8.32% from the end of the first quarter. In contrast, export module prices have remained relatively stable. OPIS assessed free on board (FOB) China TOPCon module spot prices at $0.117/W on May 12, representing only a 2.5% decline over the same period.

Although export demand weakened following the cancellation of China’s solar export tax rebate in April, leading manufacturers have largely resisted further price reductions. Geopolitical uncertainties and trade-related risks have also contributed to an “uncertainty premium” in longer-dated module orders.

Geopolitical restructuring

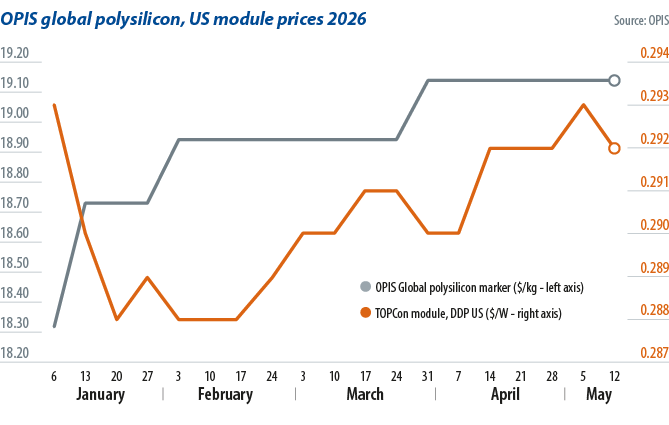

Alongside the temporary equilibrium emerging within China’s photovoltaic supply chain, overseas solar supply chains are exhibiting signs of a similar short-term balance. The Global Polysilicon Marker (GPM) – the OPIS benchmark for polysilicon produced outside China – was assessed at $19.138/kg, or $0.040/W, as of May 12, unchanged since the end of the first quarter.

Global polysilicon market fundamentals remain broadly stable, although regional pricing dynamics continue to diverge amid increasingly fragmented trade flows. US-origin polysilicon continues to trade at relatively elevated spot prices in the mid-$20/kg range, while material from other regions generally remains below $20/kg.

Spot trading activity globally remains limited. Most US-origin polysilicon volumes are tied to long-term contracts, while buyers outside the US remain cautious amid uncertainty regarding future US market access for products manufactured using non-US polysilicon.

Against the backdrop of geopolitical restructuring, polysilicon sourcing strategies are becoming increasingly diversified. A newly commissioned polysilicon facility in Oman is undergoing customer qualification processes, and a Netherlands-based polysilicon project recently received designation as a strategic initiative under the EU’s Net-Zero Industry Act (NZIA).

Import tariffs

Global polysilicon development presently remains highly dependent on whether downstream products can access the US market as US trade policy continues to exert substantial influence on global polysilicon pricing and investment decisions.

On April 23, the US Department of Commerce released preliminary antidumping determinations – largely as anticipated – with preliminary cash deposit rates set at 123.04% for Indian imports, 22.46% for Laotian imports and 35.17% for Indonesian products. However, most market participants viewed the announcement as largely anticipated.

OPIS assessed delivered duty paid (DDP) US TOPCon module prices at $0.292/W as of May 12, unchanged from April 14. Indian cargoes were stable at $0.332/W, while Southeast Asian cargoes were assessed at $0.280/W, up slightly by 0.36% over the same period.

An investigation instigated by solar manufacturers operating in the United States into rapidly rising solar imports from Ethiopia is increasing uncertainty as trade risks continue to expand geographically.

Market participants noted that only manageable final tariff determinations will enable local manufacturing operations to support additional demand for globally polysilicon from compliant supply chains.

About the author

The post Polysilicon prices in a fragile balance appeared first on pv magazine Global.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

Comments (0)