Renewable Focus

Breaking News

- RPSG’s clean energy arm to acquire ReNew’s 1.4 GW solar portfolio for ₹4,859 crore

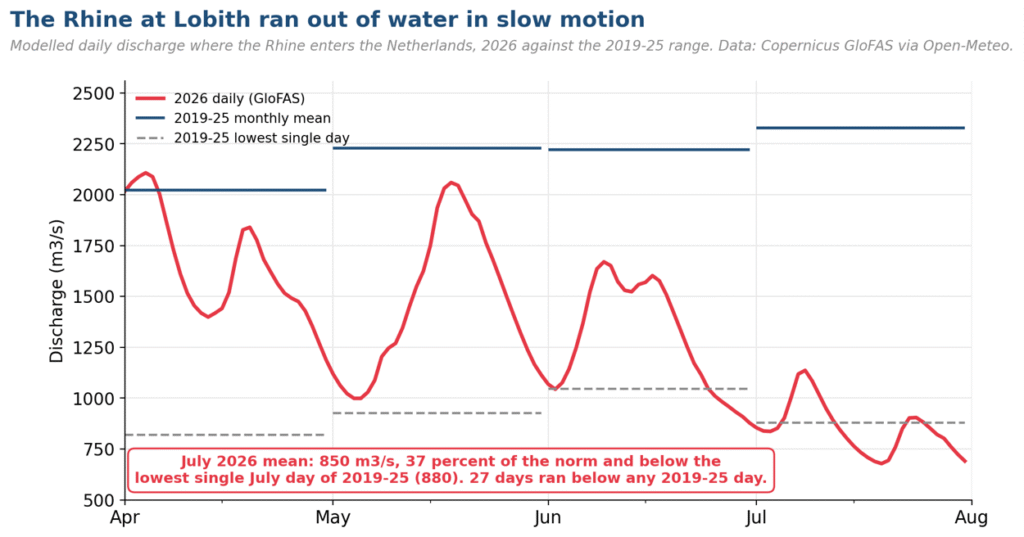

- When the rivers stop flowing: Europe’s drought summer measured

- Casella Waste Systems and Waga Energy start up Hyland Landfill RNG facility

- Waaree Energies Subsidiary Acquires 24.21% Stake in Eppeltone Engineers for Rs. 21.78 Crore

- Coal India Starts Commercial Operations Of 200 MW Solar Project In Gujarat’s Khavda

- Founder Energy Secures RM4.7 Million Contract for 1.4 MW Rooftop Solar Project in Malaysia

- Here’s our first look at the Range Rover GT in real life [Video]

- Lexus undercuts luxury rivals with 2027 ES prices starting under $50,000

- GM makes charging easy while Elon bets big on fossil fuels and Leno talks Tesla

- Clearmind Medicine to get into the wireless EV charging game

- Webinar: Thermal and climate management for off-highway EVs

- Mitsubishi confirms its first new EV in Australia for more than a decade, with VR-e electric SUV arriving this year

- GAC offers shorter-range and smaller battery Aion UT as battle for Australia’s cheapest EV heats up

- BYD officially launches upgraded Atto 3, with faster charging and more range, in NZ market

- Transit Agencies Continue to Grow U.S. Fuel Cell Bus Fleets

Solar Energy

Wind Energy

Hydrogen

Sea (Marine) Energy

EV & Hybrid

![Pony.ai to put 100,000 autonomous electric trucks on the road by 2030 [video]](https://electrek.co/wp-content/uploads/sites/3/2026/08/pony_ai.jpg?quality=82&strip=all&w=1600)

Energy & Storage

Latest Posts

View All Posts

Solar Energy

RPSG’s clean energy arm to acquire ReNew’s 1.4 GW so...

The acquisition has been funded by the parent company and is structured acros...

Solar Energy

When the rivers stop flowing: Europe’s drought summe...

River-flow, generation and price data from April to July 2026 point to a drou...

Sea (Marine) Energy

Casella Waste Systems and Waga Energy start up Hylan...

In the United States (US), Casella Waste Systems Inc., a regional solid waste...

Solar Energy

Founder Energy Secures RM4.7 Million Contract for 1....

Founder Energy Sdn Bhd has secured a RM4.7 million contract to develop a 1.4 ...

Solar Energy

Coal India Starts Commercial Operations Of 200 MW So...

Coal India Limited (CIL) has launched 200 MW of solar power capacity in Khavd...

Solar Energy

Waaree Energies Subsidiary Acquires 24.21% Stake in ...

Waaree Smart Meters Private Limited has acquired a 24.21% equity stake in Epp...

EV & Hybrid

GM makes charging easy while Elon bets big on fossil...

On today’s super simple episode of Quick Charge, we talk about GM’s new Energ...

EV & Hybrid

Lexus undercuts luxury rivals with 2027 ES prices st...

The all-electric 2027 Lexus ES returns for the 2027 model year, with prices s...

EV & Hybrid

![Here’s our first look at the Range Rover GT in real life [Video]](https://electrek.co/wp-content/uploads/sites/3/2026/08/Range-Rover-GT-first-look.jpeg?quality=82&strip=all&w=1400)

Here’s our first look at the Range Rover GT in real ...

Range Rover is adding a fifth member to its lineup, but this one is a bit of ...

Hydrogen

Transit Agencies Continue to Grow U.S. Fuel Cell Bus...

by Jennifer Gangi August 10, 2026 Fuel cell buses are not new to the transit ...

EV & Hybrid

Webinar: Thermal and climate management for off-high...

Electrifying off-highway equipment requires engineers to use a different mind...

EV & Hybrid

BYD officially launches upgraded Atto 3, with faster...

BYD launches new Atto 3 Evo in New Zealand, which will feature faster chargin...

EV & Hybrid

GAC offers shorter-range and smaller battery Aion UT...

GAC will add a shorter-range AION UT to its Australian line-up later this yea...

EV & Hybrid

Mitsubishi confirms its first new EV in Australia fo...

Mitsubishi is returning to the Australian EV market with the ASX VR-e electri...

EV & Hybrid

Clearmind Medicine to get into the wireless EV charg...

Clearmind Medicine is “a clinical-stage biotech company focused on the discov...

Solar Energy

Solar powers non-fossil capacity past 300 GW

Solar accounted for 164.59 GW of this, followed by wind (58.14 GW) and large ...